TUTORIAL 4:

FINANCIAL PLANNING FOR EXTENDED LIFE

Traditional financial planning assumes you will retire at 65 and die by 85. This model was built for a world where aging was inevitable and healthspan was fixed.

If LEV is achieved, you could live in good health for 100+ years. The question is no longer "how do I afford 20 years of retirement?" but "how do I build capital that lasts indefinitely?"

THE INSOLVENCY GAP

The Insolvency Gap is the financial equivalent of the Death Gap. It occurs when you outlive your money while still in functional health.

Standard retirement models allocate capital based on actuarial life expectancy. A 65-year-old with $2M in savings plans for 20 years of withdrawals. At 4% annual drawdown ($80k/year), the capital lasts until age 85. This works if you die on schedule.

But if LEV extends your healthy lifespan to 110, you run out of money at 85 and face 25 years of financial insolvency while biologically capable of earning, traveling, and consuming. This is a planning failure, not a longevity failure.

The Math of Extended Life

If you retire at 65 with $2M and live to 110 (45 years), you can only withdraw $44k/year at 0% real returns. Adjusted for 3% inflation, your purchasing power drops by 73% by age 110.

The traditional 4% rule assumes death at 85. Apply it to a 110-year lifespan and you become insolvent at age 85—precisely when traditional planning expected you to die.

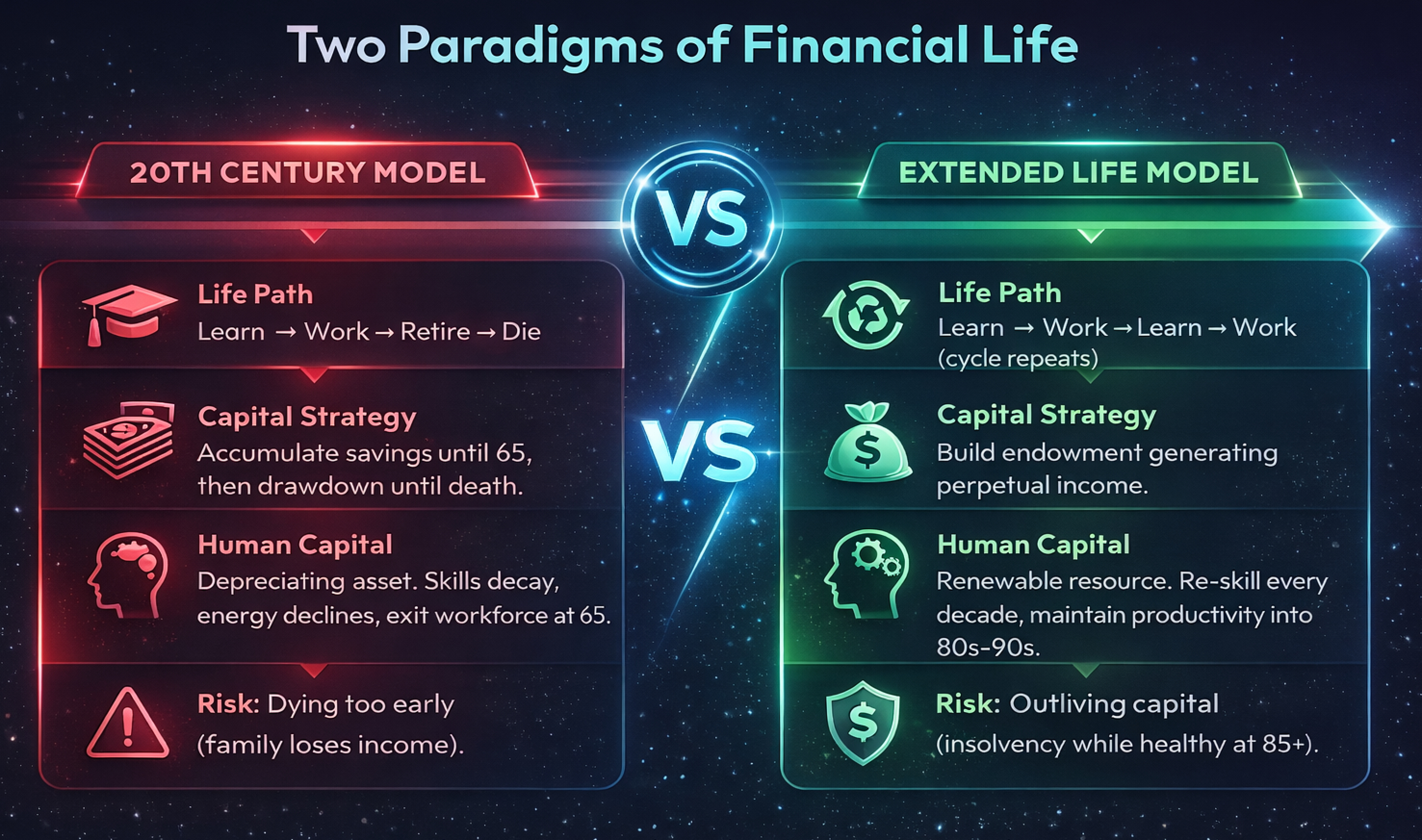

THE OLD MODEL VS. THE NEW MODEL

This visual captures the fundamental shift required for extended longevity financial planning:

20th Century Model: Linear Decline

- Life Path: Learn → Work → Retire → Die. Education ends at 22, career spans 40 years, retirement consumes savings, death terminates the plan.

- Capital Strategy: Accumulate savings until 65, then execute systematic drawdown until death around 85.

- Human Capital: Depreciating asset. Skills decay, energy declines, forced exit from workforce at 65.

- Primary Risk: Dying too early and leaving family without income support.

Extended Life Model: Renewable Cycles

- Life Path: Learn → Work → Learn → Work (cycle repeats). Education is continuous, multiple 20-year careers possible, retirement becomes optional.

- Capital Strategy: Build endowment generating perpetual income. Live on yield, preserve principal indefinitely.

- Human Capital: Renewable resource. Re-skill every decade, maintain productivity into 80s-90s through extended healthspan.

- Primary Risk: Outliving capital—insolvency at 85+ while biologically healthy and functional.

THE FIVE FINANCIAL RISKS OF EXTENDED LIFE

Longevity introduces asymmetric financial risks that traditional models ignore:

1. Insolvency Risk

Outliving your capital while still healthy and functional. The consequences compound: no income, rising healthcare costs, loss of autonomy, and inability to access longevity therapies.

2. Healthcare Cost Explosion

The last 2 years of life often cost more than the first 50 combined. Extending life without health creates a "disability tail" that destroys accumulated wealth through catastrophic expenses.

3. Inflation Erosion

A 3% inflation rate cuts purchasing power in half every 24 years. Living 60+ years in retirement means your $100k/year income becomes $25k in real purchasing power by age 110.

4. Skill Obsolescence

Your degree at 22 is irrelevant by 50. In a 100-year life, you must retool every 15-20 years or become economically obsolete while biologically capable of productive work.

5. Sequence-of-Returns Risk

A market crash at age 70 that depletes capital by 40% leaves you with 40+ years to recover. Traditional retirees die before sequence risk fully manifests over decades.

THE ENDOWMENT MODEL

The solution is to stop planning for drawdown and start building an endowment—a capital base that generates income indefinitely while preserving principal.

Principles of Endowment Planning

- Live on yield, not principal: Target 3-4% sustainable withdrawal from dividends, interest, and growth. Never touch the capital base itself—preserve it perpetually.

- Inflation-adjust perpetually: Your endowment must grow at the rate of inflation or faster. Real returns above inflation fund your life; inflation protection preserves purchasing power across decades.

- Diversify across time: Allocate to assets that perform in different economic regimes—stocks, real estate, commodities, inflation-protected securities, longevity biotech equity.

- Plan for multiple earning phases: Assume 2-3 distinct careers over your extended lifespan. Human capital supplements and extends financial capital.

The New Retirement Equation

Traditional model: Savings ÷ Years until death = Annual spend

Endowment model: (Endowment × Yield) + (Human Capital × Productive Years) ≥ Annual spend × Inflation

This changes the question from "How much do I need to retire?" to "How much do I need to generate sustainable income forever?"

Example: The $3M Threshold

At a 4% real yield, a $3M endowment generates $120k/year indefinitely. If you can live on $120k (adjusted for inflation annually), you have solved the insolvency problem permanently.

If your expenses are $150k/year, you need either $3.75M in capital or $30k/year in supplemental income from part-time work, consulting, or royalties. Extended healthspan makes earning at 75 entirely feasible.

HUMAN CAPITAL AS A RENEWABLE RESOURCE

Extended healthspan reframes human capital. Instead of a single 40-year career followed by permanent exit, you have multiple 15-20 year career arcs spanning different industries and expertise domains.

The Multi-Stage Career Model

- Stage 1 (Age 22-45): Build foundational expertise, earn aggressively, accumulate seed capital. Focus on high-income skill development and capital formation.

- Stage 2 (Age 45-65): Leverage accumulated experience, transition to advisory/ownership roles, reduce time commitment while maintaining income. Build passive revenue streams.

- Stage 3 (Age 65-85): Retool into adjacent field (e.g., engineer → biotech consultant), work part-time on passion projects, supplement endowment income. Maintain cognitive engagement.

- Stage 4 (Age 85+): Optional continued work, royalties, board seats, or full leisure funded by endowment. Financial independence achieved through Stages 1-3.

Each stage compounds the previous. Stage 1 builds financial capital. Stage 2 converts time into equity. Stage 3 leverages accumulated expertise for high-value, low-time-commitment work. Stage 4 is optional because Stages 1-3 secured the endowment.

LONGEVITY-SPECIFIC INVESTMENTS

If you believe LEV is achievable, allocating capital to longevity biotech creates a powerful hedge: if the therapies succeed, your health benefits and your portfolio appreciates. If they fail, you needed aggressive life extension anyway, so the financial loss becomes secondary.

Consider allocating 5-15% of growth capital to:

- Longevity biotech ETFs or index funds tracking anti-aging companies

- Direct equity in companies developing senolytics, gene therapies, or cellular rejuvenation

- Real assets (real estate, commodities) that hedge inflation over 50+ year investment horizons

- Healthcare REITs and senior living facilities positioned for demographic shifts

THE STRATEGIC SHIFT

Financial planning for extended life requires a fundamental mindset change:

- Stop optimizing for "enough to retire at 65." Optimize for "enough to sustain indefinitely."

- Stop treating age 70 as "too old to work." Treat it as mid-career if healthspan extends to 100+.

- Stop withdrawing principal from your capital base. Build systems that generate perpetual income streams.

- Stop planning for one life phase. Plan for 3-4 career reinventions across multiple decades.

The Insolvency Gap is as dangerous as the Death Gap. Reaching LEV while financially insolvent is a failure state. Financial resilience and biological resilience must be planned in parallel—neither alone is sufficient.

Assess Your Resilience

Test your assumptions with the Longevity Horizon Quiz, then use Functional Resilience to measure your capacity to sustain productivity and health into extended lifespan.

Take The Quiz Check Functional ResilienceGet The Full Financial Strategy

The 2026 Longevity Horizon Report includes financial modeling frameworks for extended lifespan, capital allocation strategies, and human capital optimization across multiple career stages.

Get The 2026 Report